DEMYSTIFIED INVESTING IS FUN.

START INVESTING IN YOURSELF TODAY.

Enter your mail to get the latest dose of investing insights to your inbox, delivered weekly.

Explore

Mindsets

Master the right investing mindsets and develop powerful habits to become a successful Passionate Investor.

Stock Market

Invest in stocks, bonds, ETFs and mutual funds for a diversified portfolio and hedge against risks.

Real Estate

Invest in different types of real estate and learn about real estate investing strategies that work for you.

Alternative Assets

Invest in cryptocurrency, fine art, and other alternative assets in which you can combine your interests and creative investing strategy.

Collaborate

Interested in working together on your next real estate project? We provide consulting services for investors and developers.

- Market Analysis

- Feasibility Study

- Deal Analysis

- Cash Flow & Revenue Analysis

- Business Plan

- Pitch Deck

- ……

- We can customize the service based on your project and needs. Contact at x.vanessamao@kw.com

Invest in Yourself First

Then invest in assets

The most important investment you should make in your life is yourself – your mindset, health, character and relationships. As you are working towards a whole soul, you will have the confidence and the grit to tackle challenges in life and work.

A diversified portfolio of different assets including stocks, real estate and other alternative investments is key to build your freedom. Everyone’s investment portfolio mix is different and the best one is the one that fits your dream lifestyle.

Start exploring here

-

7 Best Creative Financing Stratgies for Real Estate Investors

Innovative investors often leverage creative financing techniques to expand their opportunities. Here are the 7 best creative financing strategies for real estate investors:

- Seller financing and lease options

- Subject to deals

- Real estate partnerships and joint ventures

- Creative use of home equity and HELOCs

- Crowdfunding and real estate syndication

- Self-directed IRAs and retirement funds

- Peer-to-peer lending platforms

In this article, we’ll delve into seller financing, lease and subject to options, which can provide flexibility and unique advantages. Additionally, real estate partnerships and joint ventures enable investors to pool resources, knowledge, and experience to achieve remarkable outcomes. We also explore how tapping into home equity and utilizing home equity lines of credit (HELOCs) can be strategic approaches to finance your real estate endeavors.

There are more alternative financing sources has opened new doors for real estate investors. Crowdfunding and real estate syndication platforms offer opportunities to invest in properties collectively, diversifying risk and potentially accessing larger-scale projects. Self-directed IRAs and retirement funds provide avenues for investing in real estate tax-efficiently. Moreover, peer-to-peer lending platforms present alternative funding options for those seeking more unconventional paths.

Photo by Pixabay on Pexels.com 1. Seller financing and lease options

First, seller financing and lease options are two powerful creative financing techniques that real estate investors can leverage to achieve their investment goals. Seller financing involves the property owner acting as the lender, allowing the buyer to make payments directly to them instead of securing a traditional mortgage. This arrangement can be advantageous for both parties, as it eliminates the need for a bank or financial institution and allows for more flexible terms and negotiation.

On the other hand, lease options provide investors with the opportunity to control a property without necessarily owning it. In a lease option, the investor leases the property from the owner with the option to purchase it at a predetermined price and time in the future. This approach allows investors to generate cash flow from the property while having the potential to acquire it at a later date. Seller financing and lease options offer creative ways to structure real estate transactions, providing investors with greater flexibility and opportunities for profitability.

2. Subject to deals

Second, subject to deals are a creative financing technique that can offer real estate investors unique opportunities to acquire properties without assuming the existing mortgage. In a subject to deal, the investor purchases the property “subject to” the existing mortgage, meaning they take over the mortgage payments and responsibilities while the loan remains in the seller’s name. This arrangement allows investors to bypass the need for traditional financing and potentially acquire properties with little to no money down.

However, it’s crucial to thoroughly analyze the terms of the existing mortgage and assess the risks involved. Subject to deals can be a win-win for both parties, as sellers are relieved of the burden of their mortgage while investors gain control of a property with favorable terms. By understanding the intricacies of subject to deals and conducting proper due diligence, investors can leverage this creative financing technique to expand their real estate portfolio and maximize their returns.

3. Real estate partnerships and joint ventures

Real estate partnerships and joint ventures are powerful creative financing techniques that allow investors to pool resources, knowledge, and experience to achieve remarkable results. By partnering with others in the real estate industry, investors can tap into a wider range of expertise and capital, enabling them to pursue larger and more lucrative investment opportunities.

In a real estate partnership, two or more parties come together to jointly invest in a property or a series of properties. Each partner contributes funds, skills, or other resources in proportion to their agreement.

Joint ventures, on the other hand, involve collaborating with other investors or entities to undertake a specific real estate project. These collaborative arrangements not only distribute financial risks but also provide access to a broader network and shared responsibilities.

Successful real estate partnerships and joint ventures require clear communication, well-defined roles, and a mutually beneficial agreement. By harnessing the power of collaboration, investors can unlock the potential for greater success and profitability in their real estate endeavors.

Photo by Timur Saglambilek on Pexels.com 4. Home equity and HELOCs

Home equity and Home Equity Lines of Credit (HELOCs) are valuable tools within the realm of creative financing for real estate investment. Home equity refers to the portion of a homeowner’s property value that exceeds the outstanding mortgage balance. By tapping into their home equity, investors can access funds for real estate investment purposes.

One popular method is through a HELOC, which functions as a revolving line of credit secured by the equity in one’s home. Investors can borrow against their home equity as needed, making it a flexible financing option. Home equity and HELOCs enable investors to leverage their existing property assets without needing to secure additional mortgages or loans.

However, it’s important to carefully assess the risks and obligations associated with using home equity, as defaulting on HELOC payments can result in foreclosure. By understanding the potential benefits and risks, real estate investors can utilize home equity and HELOCs strategically to fund their ventures and unlock new investment opportunities.

5. Crowdfunding and real estate syndication

Crowdfunding and real estate syndication are innovative financing techniques that have gained popularity in the real estate investment landscape. Crowdfunding platforms allow multiple investors to pool their funds and collectively invest in real estate projects.

Real estate syndication, on the other hand, involves forming a group of investors who collectively invest in larger-scale properties or development projects. These strategies are ideal for real estate investors who want to diversify their portfolios, access larger and more lucrative projects, and mitigate individual risk.

Crowdfunding and real estate syndication provide opportunities for passive investors to participate in real estate without the need for extensive knowledge or direct involvement in property management. Additionally, these financing techniques are suitable for ambitious development projects that require substantial capital beyond what a single investor can provide. By embracing crowdfunding and real estate syndication, investors can access a wider range of opportunities and potentially benefit from professional management and shared risk.

6. Self-directed IRAs and retirement funds

Self-directed IRAs and retirement funds offer investors a unique avenue for financing real estate investments. With a self-directed IRA, investors have the freedom to direct their retirement funds into a wide range of investment options, including real estate. By utilizing these funds, investors can access tax advantages and potentially grow their retirement savings through real estate appreciation, rental income, or property development. This creative financing technique allows investors to diversify their retirement portfolios while gaining exposure to the lucrative world of real estate.

However, it’s important to adhere to IRS regulations and work with a custodian experienced in self-directed IRAs. Self-directed IRAs and retirement funds are ideal for investors seeking long-term growth and a tax-efficient way to invest in real estate. By leveraging these funds, investors can combine the benefits of real estate investments with the potential for retirement savings growth, making it a compelling option within the realm of creative financing techniques for real estate investment.

Photo by Monstera on Pexels.com 7. Peer-to-peer lending platforms

last but not least, peer-to-peer lending platforms have emerged as a dynamic and accessible creative financing technique for real estate investment. These platforms connect borrowers, typically real estate investors, directly with individual lenders, cutting out traditional financial institutions.

Through peer-to-peer lending, real estate investors can secure funding for their projects quickly and efficiently. This strategy is particularly suitable for investors who may face challenges in obtaining financing through conventional channels, such as strict credit requirements or limited borrowing options. Peer-to-peer lending offers a streamlined and flexible alternative, providing opportunities for investors with various credit profiles or unconventional real estate projects.

Additionally, this financing technique is beneficial for investors seeking more control over loan terms and interest rates, as it allows for negotiation and customized agreements. By leveraging peer-to-peer lending platforms, real estate investors can access capital, seize investment opportunities, and diversify their funding sources, making it an attractive option within the realm of creative financing techniques for real estate investment.

Summary

Mastering the best real estate investment financing tactics is a game-changer for investors. When choosing the best creative financing strategy, real estate investors should consider factors such as their investment goals, risk tolerance, financial capabilities, property type, market conditions, and time horizon. Evaluating these factors helps investors align their creative financing strategy with their specific needs and preferences.

Additionally, conducting thorough research, analyzing the costs and benefits of each strategy, and seeking professional advice can aid investors in making informed decisions. By carefully considering these factors and selecting the most suitable financing strategy, real estate investors can optimize their investment opportunities, manage risks effectively, and maximize their returns.

Disclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational and entertainment purposes only. Read our full disclaimer here.

-

6 Best Property Analysis Tools for Real Estate Investors

Real estate investment is a complex process that requires careful analysis and research. To make informed decisions, investors should have access to the right tools. These tools range from investment property analysis software to rental property analysis tools, from cash flow calculators to rehab calculators, and more. With the right combination of these tools, investors can gain valuable insights into the future financial performance of an investment property and chase the right deals.

This article features several affiliate links, meaning we may receive a small affiliate commission if you purchase through these links.

Here are our picks for top property analysis tools in 2023:

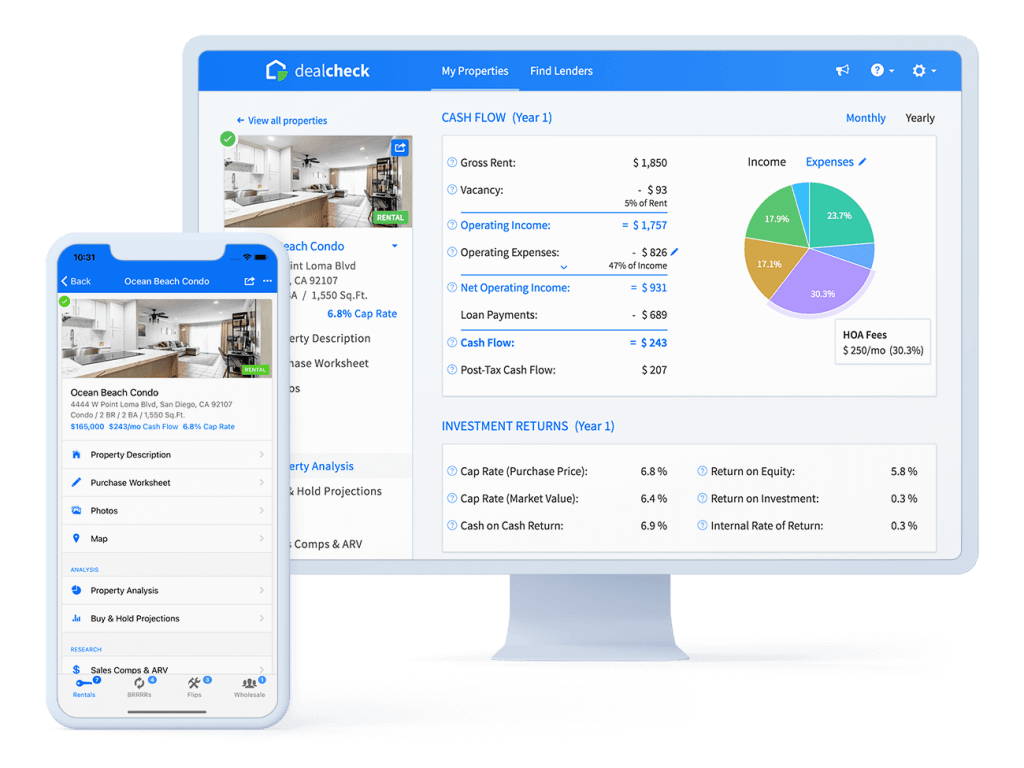

1. DealCheck: Most Easy to Use

DealCheck is a powerful real estate investment tool that helps investors quickly analyze and compare potential investments. With a comprehensive set of features, DealCheck provides investors with an easy-to-use platform for analyzing and comparing properties to find the best investment opportunities. The tool provides users with detailed analysis of potential investments, including rent estimates, cash flow forecasts, and other important metrics.

Features include:

- Calculate all important metrics for rentals, BRRRR’s, flips, multi-family, commercial buildings and Airbnb’s in seconds.

- Quickly search public records & online listings and import property details, list price, estimated value & rent, property taxes, HOA fees and photos.

- Analyze long-term cash flow projections for rental properties and profit projections for flips.

Pricing:

- Starter: FREE

- Plus: $10/ month billed annually

- Pro: $20/ month billed annually

Special Promotion:

- 20% Off when you use PASSIONATE promo code

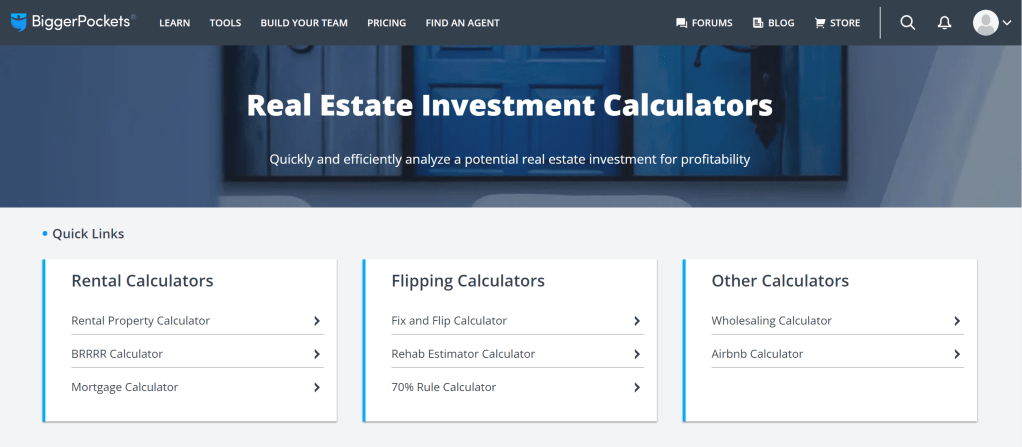

2. BiggerPockets

BiggerPockets is a complete resource for real estate investors. It provides content, tools, and a community of real estate investors who share valuable advice and tips from their investment stories. BiggerPockets offers 8 different calculators including rental and flipping calculators.

Features include:

- Quickly and efficiently analyze a potential real estate investment for profitability using 8 calculators of different strategies.

- Should you experience any difficulty with the calculators, or run into any issues with your report, there is a customer support team and community you can reach out to.

Pricing:

- Starter: FREE for first 5 reports

- Pro Monthly: $39/ month

- Pro Annually: $32.5/ month billed annually

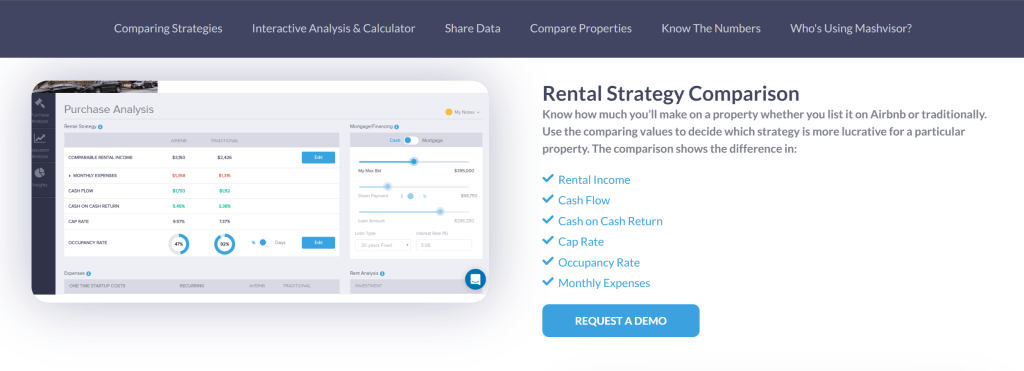

3. Mashvisor: Best for Strategy Comparison

Mashvisor’s Investment Property Tool is designed to provide investors with an in-depth analysis of potential investments, allowing them to make more informed decisions. With the help of this tool, users can quickly and accurately evaluate rental properties, compare different neighborhoods, and generate accurate rental returns. The tool also provides users with important insights into the local market conditions and trends. This makes it easier for investors to assess the profitability of a potential investment before investing.

Features include:

- Know and compare rental strategy by looking at how much you’ll make on a property whether you list it on Airbnb or traditionally.

- With its interactive Purchase Analysis and Investment Property Calculator, you can personalize the property by giving it your own personal rating and making your own notes.

- Gain perspective on an overall evaluation of the neighborhood, the property, and the Airbnb market.

Pricing:

- FREE for 7 days

- Lite: $17.99/ month billed annually

- Standard: $49.99/ month billed annually

- Professional: $74.99/ month billed annually

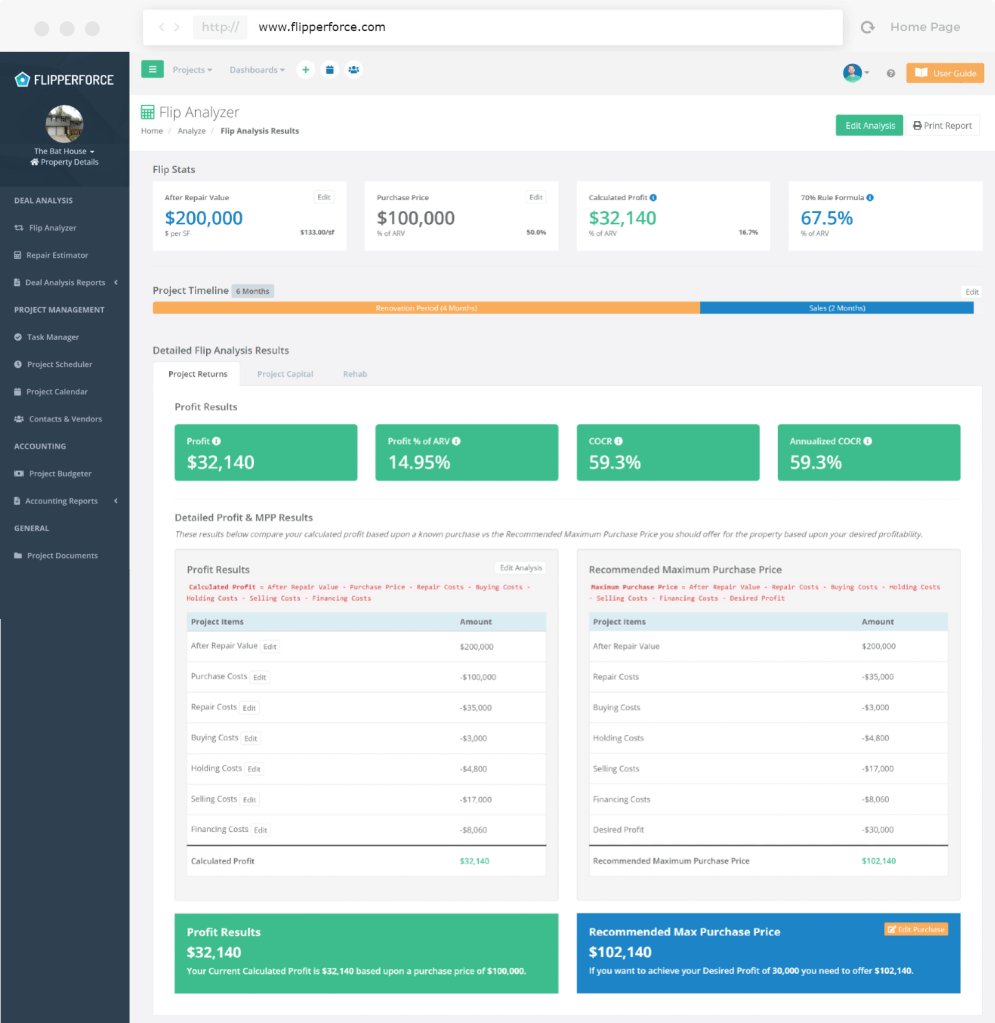

4. FlipperForce: Best for Flipping

FlipperForce is an all-in-one web-based house flipping software built to help house flippers, rehabbers & investors analyze deals & manage their rehab projects. FlipperForce offers deal analysis tools and house flipping calculator which allows investors to evaluate potential deals and determine the maximum purchase price that should be offered for the property. With a focus on flipping and BRRRR strategy, FlipperForce can help investors take their rehab projects into the next level of excellence.

Features include:

- Analyze House Flips & BRRRR Deals, Estimate Rehab Costs and Create Professional Investment Reports to Raise Funding for your Flips.

- Manage Your Rehab Project Calendars, Project Schedules, Tasks and To-Dos to Keep Your Rehab Projects on Track.

- Manage Your Project Budgets, Track Project Expenses & Forecast Profitability to stay on Budget

Pricing:

- 30 day FREE trial

- Solo: $59/ month billed annually

- Team: $149/ month billed annually

- Business: $349/ month billed annually

5. DealCrunch

Made by real estate investors, for real estate agents, lenders, brokers or anyone who is just starting out with real estate investing, DealCrunch takes real estate analysis to the next level. This mobile-focused app provides you with the simplest and most intuitive user experience that can help you analyze rental property, rehab renovation projects as well as other investment types.

Features include:

- Analyze all sorts of investment properties: single-family rental, multi-family rental, vacation rental, rehab project, fix and flip, commercial real estate and much more.

- Calculate cash flow and other financial metrics easily: capitalization rate (cap rate), cash on cash return (COC), return on investment (ROI) and more.

- View and share in-depth property analysis summary and visualize long term holding projections and profitability.

- Connect with other investors and discuss your recent deals.

Pricing:

- Bronze: FREE

- Gold Monthly: $8.99/month

- Gold Yearly: $89.99/year

6. Roofstock: Most Straightforward

Check out Roofstock’s free and simple rental property analysis spreadsheet. If you are old fashioned and prefer a simple, easy-to-use spreadsheet, this one’s for you. This spreadsheet allows you to browse all inputs, assumptions, results and purchase metrics in one page. After all, making sense of the numbers behind real estate investments does not need to be complicated.

Features include:

- Have all inputs, assumptions and results in one page.

- Show different purchase criteria in one place, including Cap Rate, Monthly Cash Flow and CoC etc.

Summary

Photo by Mikhail Nilov on Pexels.com Investing in a property that isn’t profitable is an expensive mistake that can cost real estate investors time and money.

Rental property analysis tools can help you choose the right properties to invest in. These tools provide insights into what kind of income a given property is likely to generate, as well as estimated rent prices and vacancy rates. Try these tools and find the ones that work best for you.

Disclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational and entertainment purposes only. This article features several affiliate links, meaning we may receive a small affiliate commission if you purchase through these links. Read our full disclaimer here.

Subscribe for our latest insight in investing and building financial freedom.

-

3 Best Ways to Manage Your Emergency Fund

Introduction: What is an Emergency Fund and Why Should You Have One?

An emergency fund is money set aside to cover unexpected expenses or income shortfalls that arise during times of financial difficulty. It can be used to pay for medical bills, car repairs, job loss, or other unexpected costs. Having an emergency fund can help you avoid taking on debt and provide peace of mind knowing you have a safety net when life throws a curveball.

Photo by Andrea Piacquadio on Pexels.com There are several ways to save money for your emergency fund such as setting up automatic transfers from your paycheck or opening a high-yield savings account with an online bank. In this article, we will talk about some of the best options to store and manage your emergency fund.

Best Ways to Store Your Emergency Fund

The best ways to store your emergency fund are through a high yield savings account, money market fund, or an emergency savings account. These accounts offer higher interest rates than traditional bank accounts and provide easy access to your funds when needed. Additionally, these accounts are FDIC insured which offers additional protection for your funds. Let’s look at these accounts in more details:

- High yield savings account

A high yield savings account is a type of savings account that provides competitive interest rates on your deposited funds. This type of account is FDIC insured, which means that your funds are protected up to $250,000 in case the bank goes out of business. It is a great way to store an emergency fund, as it allows you to earn more money while keeping your money safe and secure.

High yield savings accounts offer higher interest rates than traditional savings accounts, so you can maximize the return on your money while still having access to it when needed. They also provide liquidity and easy access to your funds in case of an emergency. With competitive interest rates and FDIC insurance, high yield savings accounts are a great choice for storing your emergency fund.

- Money market fund

Money market funds are a type of fixed income mutual fund that invests in short-term debt instruments with high credit quality. They provide investors with a low risk and more accessible way to store emergency funds.

Money market funds are known for their low volatility and short maturities, making them an ideal choice for investors looking to preserve capital while earning a competitive return. These funds also provide the added benefit of liquidity, allowing investors to access their money quickly if needed. Therefore, money market funds are also an ideal option to park your emergency fund while making a return.

- Cash or Checking Account + short-term CDs

Simply storing your emergency fund in only a cash/checking account or only in a CD account might not be wise since an everyday checking account offers very low interest rates and a CD account adds illiquidity to your emergency fund unless you pay a penalty for any early withdrawal of the funds. But how about a combination of these?

For example, you could store a portion of your emergency fund in a checking account for liquidity while storing the rest in a short-term CD (for example, a 3-month CD) to get the best of both worlds.

Of course, you could allocate your emergency fund across all of the accounts mentioned above or focus on one strategy. Remember, it is only used for emergencies; thus safety and liquidity of the funds should be our priorities when managing this fund.

Last thoughts

Photo by Revathi Seraman on Pexels.com Knowing when and how often to use your emergency fund can help you make the most of it and ensure that you don’t run out of money when you need it most. By having an emergency fund in place, you will be better prepared for any unexpected financial emergencies that may arise in the future.

It is also important to adjust your emergency fund amount as our life situations change. For example, as we age, we might encounter more, bigger unexpected medical bills; in this case, we might want to save a greater reserve to battle these emergencies.

“Life is like a box of chocolates, you never know what you’re going to get.” If you get a bitter one, at least you have an emergency fund to buy another box.

Forrest Gump & The Passionate InvestorDisclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational and entertainment purposes only. Read our full disclaimer here.

Subscribe for our latest insight in investing and building financial freedom.

-

Plan Your Money in Four Big Buckets

Financial planning is an important part of building financial freedom. It involves making wise decisions about your money and investing it in different time horizons, such as short-term, mid-term, and long-term investments. By separating funds into different buckets of investments based on time horizons, you can ensure that your money works for you in every stage of life.

Photo by Karolina Grabowska on Pexels.com Here are the Four Buckets of Money you can plan for (you could adjust the timelines based on your own unique situation and needs):

#1 Bucket: Emergency fund

An emergency fund, also known as a rainy day fund, can provide you with the peace of mind that you are prepared for any financial situation. It can be used to pay for medical bills, car repairs, or any other unexpected costs that may arise. Moreover, it will give you the security to know that if your income suddenly drops due to job loss or other circumstances, you have money set aside to help get through it.

Having an emergency fund is one of the most important aspects of personal finance. It is a financial safety net that can help you cover unexpected expenses and weather through economic downturns such as recessions.

It is widely recommended to have enough savings to cover at least 3 to 6 months of living expenses in order to prepare for any potential rainy day scenarios. Therefore, an emergency fund is your first bucket of money to set aside and you want to keep it rather liquid by storing it in a high-yield savings account or some other liquid accounts.

#2 Bucket: Money for the next 6-12 months

The second bucket of money to consider is your living expenses for the foreseeable future – it could be 3, 6, or 9 months, depending on your comfort level and time horizons. You would want to give yourself a peace of mind that you are able to cover your living expenses especially during a volatile economy.

The key is to create a budget that is tailored to your needs. This means taking into account all of your living expenses for the next months, as well as potential investments you may want to make in the near future. Once this budget is set, it’s important to stick to it.

With the right approach, you can ensure that you have enough money to cover your living expenses while also investing in the short term. Some of the short-term investments include CDs, high-yield savings accounts, short-term corporate and government bond funds, money market funds, treasuries and cash management accounts.

Photo by Monstera on Pexels.com #3 Bucket: Money for the next 2-5 years

Do you expect to have any major purchases for the next 2-5 years? Such as submitting a down payment for a house, purchasing a car, having a wedding or planning to have a child? Make sure you consider these significant expenditures into your financial plan.

Having these major expenditures in mind, you now want to manage and invest for the mid term. Given the longer time span, you have more creativity on how to allocate and invest the money. Consider investing in ETFs, dividend stocks and some fixed-income instruments as long as you are comfortable with the associated risks of these investments. But do be cautious that during uncertain economic times, some asset classes might lose you money – consult your wealth management advisor to choose the right products with acceptable risks.

#4 Bucket: Money for long-term investments (10-15+ years)

The final but probably the most important bucket of money is for long-term investing. Investing for the long term is a great way to build financial freedom. It allows you to take advantage of compounding, which is the process of earning returns on both your original investment and on returns you received previously.

Warren Buffett, one of the most successful investors of all time, is a huge proponent of long-term investing and has been investing for more than 80 years.

Photo by Picas Joe on Pexels.com Long-term investing certainly requires patience and discipline, but it can lead to significant returns over the course of years or decades. By taking a long-term view on your investments, you can benefit from stock appreciation as well as dividend payments. With a long-term strategy, you might look into stocks, real estate and other asset classes that tend to appreciate over time.

It is not about timing the market; it is about the time in the market.

Disclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational and entertainment purposes only. Read our full disclaimer here.

Subscribe for our latest insight in building financial freedom.

-

How to Stay Passionately Consistent

Consistency is often the key to our successes in life. Many entrepreneurs have practiced the discipline of doing things consistently to achieve their goals. Here are 6 ways to stay outrageously consistent in pursuing your most important life goals.

1. Have a big why and fully commit to it

First, you need to have a big why in your pursuit. Why will you get up early to work towards this goal? Why should you prioritize your time in doing this instead of other things? What benefits and meaning will your actions result in? Having a big why assigns purpose to your actions and brings you clarity in your daily endeavors.

For example, a lot of people attribute the pursuit of financial freedom to the love of their family and sense of responsibility. Because the happiness of family is their big why, they are able to remain unwavering and tackle challenges in their financial freedom journey.

After determining on the goal on which you have a big why, then you fully commit yourself to it. By being mentally all in, you don’t waste time negotiating with yourself out of work. You are your biggest enemy in defeating fear and stagnation.

Aristotle once said, “We are what we repeatedly do.” Once you’ve built that momentum of consistently doing things that you value, they become part of your daily life, habits and your identity. And things do become easier as we are practicing consistently and make them habitual.

2. Block time to complete actionable tasks

Having a plan and breaking the goal into time-bound, actionable tasks is essential to achieve consistency.

By setting enough time aside for pursuing your priorities, you grant yourself the necessary focus to maintain consistency for quality work. In addition, when you plan the time block into your schedule, you are mentally preparing and committing yourself into the activity.

Ideally, you do it early during the day or the week. It is often easier to complete planned tasks when you have more energy and mental control during the day. Eat the frog in the morning!

Photo by Acharaporn Kamornboonyarush on Pexels.com 3. Have an accountability partner or group

When you have a partner or a group of people who share the same goal and do it together with you, it is often easier to maintain consistency in that activity. This activity becomes bigger than you or any member from your group. People are counting on you to show up.

For example, to gain consistency in playing tennis, you may consider finding a tennis partner or joining a community that practices every week – you might feel obligated to go because your partner and group are expecting you to come.

Another way you can generate more accountability is to preset and automate the process. For example, for you to study Spanish more consistently, you sign up for a language lesson every Saturday. You pay for the lesson in advance (preset the activity) – so it is not an option not to go. If you want to invest more, you can use financial software to automatically invest a portion of your income into mutual funds each month (automate the process).

It always helps if you can find an accountability partner to join you along the journey.

4. Celebrate every win and take time to reinvigorate

When you accomplish a goal, small or big, acknowledge the win and reward yourself! This acts as reinforcement that it is meaningful you are acting consistently. It will motivate you to sustain momentum and keep going.

Remember to take time off to fully reinvigorate. Imagine your body and mind as a machine. For it to run efficiently and consistently, it needs to be oiled from time to time.

Taking care of your physical and mental health is vital for consistency in your endeavor. Fuel your mind and body for any marathon in life.

Photo by Oziel Gu00f3mez on Pexels.com 5. When times get tough, try MVE (Minimum Viable Effort)

In the startup world, MVP refers to Minimum Viable Product – “a version of a product with just enough features to be usable by early customers who can then provide feedback for future product development” according to Wikipedia.

Borrowing the concept and applying it to real life, MVE, Minimum Viable Effort, refers to just enough efforts that will generate an impact and still contribute to your goal. Of course, it’s best if you go for the extra mile every time. But when things get tough or you are having a really bad day, it is still worthwhile to pay MVE and do it anyway, even though it is not up to your usual workload or expectation.

“Showing up is half the battle”, Stephen Hawking once said. Once you decide to show up, you’ve already done MVE and it’s more likely you will do more. For example, a 15-min workout is better than no workout; once you make the decision to work out, you are more likely to work out longer.

6. Alway come back from failures and keep going

Failures are inevitable. There will be times that you miss a practice, fail a test or feel stuck. That’s okay.

But it’s always important to learn from your failures and ask: what makes me lose my consistency? Can I eliminate these distractions and factors that cause me to fail? What can I do better next time?

The key factor that separates people who succeed and who don’t is consistency. It is crucial to get up and keep going when you fall. Hopefully each time we fail better and always come back wiser.

-

Buying Your First Investment Property in 2023

If it is your first time buying an investment property, it can be daunting: What type of property should I invest in? How much should I put down as a down payment? Which neighborhood should I invest in? Is this the right market timing to invest in a property?

Before you bombard yourself with a million questions, read on the following steps for buying your first investment property with confidence.

Step 1: Determine Your Investment Goals & Strategy

Photo by fauxels on Pexels.com Perhaps the first, and the most important question, one should ask himself/herself is: Why am I investing in properties?

Some people invest in real estate for long-term appreciation and diversification of their investment portfolio. Some invest in rental properties that cash flow well and produce extra income. Others just enjoy fixing and flipping houses while making a profit of their labor and home improvement skills.

Having clarifications on your long-term investment goals and your motivation in pursuing real estate investment helps you decide on your investment strategy and achieve your objectives better.

Being one of the most illiquid, traditional assets, real estate isn’t for everyone. For example, with buy-and-hold real estate, an investor will typically purchase a property, hold it for at least 5 years or more, and then sell or refinance the property.

If you are not the patient type who can wait for 5 years or more for property appreciation, consider fix and flip. In a fix and flip scenario, it takes from 3 months to 12 months on average to finish the project and sell for a profit.

Therefore, understanding your investment style and strategy is crucial for your real estate investment endeavor.

Here are some popular real estate investment strategies:

- Buy and hold – buy a property and hold it for an extended period of time for home value appreciation (you can live in the property or rent it out)

- House hacking – buy a multifamily home, live in one unit and rent the other unit(s) out

- BRRRR – buy (a property at below-market value which you can add value by improving it), rehab, rent, refinance and repeat

- Fix and flip – buy a property at discount, fix it up and sell it for a profit

- Wholesaling – find a distressed property for sale, put it under contract, find a third-party buyer and harvest the difference in prices

- Syndication – join a group of investors pools together capital to jointly purchase a large real estate property and receive passive income

- REITs – invest in Real Estate Investment Trusts and receive dividends

You can use one or a combination of these strategies in your real estate investment portfolio. In addition, your financial situation and ability to leverage will also influence which strategies make more sense to you.

Step 2: Gauge Your Financial Situation

Photo by Mikhail Nilov on Pexels.com The next question you should ask: How much capital can you allocate into real estate deals in the next 3, 5 and 10 years? Developing a feasible financing plan lays the foundation for determining your real estate investing strategy.

If you have zero to small amounts of capital to invest in real estate, you might want to use more leverage in your investments by taking out a mortgage. Consider a VA or FHA loan which allows you to put down as little as zero to 3.5% as down payment if you qualify.

If you decide to apply for a FHA loan, check its requirements before applying. One of the important criteria for a FHA loan is that the home must be the borrower’s primary residence; with this financing method, house hacking is a great strategy for buying your first investment property.

If you have more capital to invest in properties, you can put down 20% or more as the down payment to avoid paying for PMI (Private Mortgage Insurance), a type of insurance that conventional mortgage lenders require when homebuyers put down less than 20 percent of the home’s purchase price.

If you want to avoid a mortgage and interest payments at once, there is the option to buy your first property in cash. Risky and illiquid it might seem to most investors, this all cash strategy has its own benefits – close the deal faster, no mortgage, interests or other fees and earn rental income right away.

How you should allocate your capital also depends on your investment portfolio size and timeline. But if you are unsure of your long-term goals, you can start with the financing and investment strategies for the next three years and then adjust them later as you gain more perspective and experience.

Step 3: Find Your First Investment Deal

Photo by Jopwell on Pexels.com Having your financing and investment strategies sorted out is half the success! Now you are executing your plan and vision.

As a beginner real estate investor, you might want to work with a seasoned investor-friendly agent or professional to shine some light on the deal searching process.

At the same time, learning to analyze the investment deal yourself is an important education for real estate novices. Get the math right. Calculate important investment ratios to help you evaluate the potential deals. Here are the 5 Property Investment Ratios You Should Know.

DealCheck is one great tool to analyze your first investment property. With DealCheck, you can analyze, view & compare your property analysis and financial ratios in one place:

Use the promo code PASSIONATE for 20% off when you purchase any products on DealCheck

Summary

Finding the right property to invest in isn’t gonna happen overnight – be patient, check listings and do deal analysis regularly, go to open houses, talk to real estate agents, keep a good credit score and healthy relationship with the lenders. Opportunities always present themselves to those who are prepared.

Subscribe for our latest insight in building financial freedom.

Disclaimer: The information and/or documents contained in this article does not constitute financial advice and is meant for educational and entertainment purposes only. Read our full disclaimer here.

About

Hi! I’m Vanessa Mao, the founder of The Passionate Investor. I am passioante about investing and connecting with like-minded people.

I invite you to join us on the journey of personal growth and wealth building. Start investing today for a better future.

Email: x.vanessamao@kw.com